Your Business and Industry

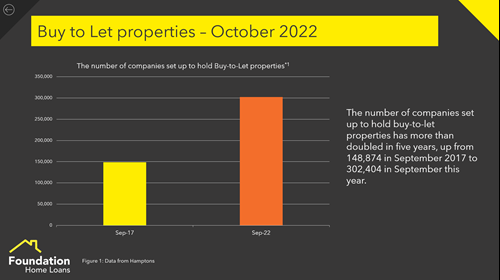

SPVs for buy to let doubled in 5 years

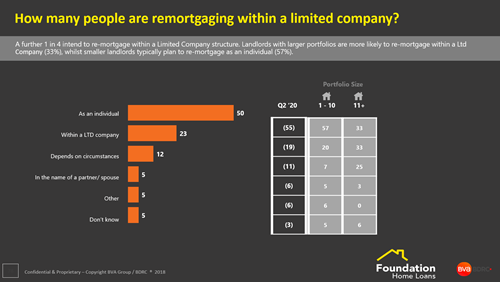

Buying this way is popular, but how many landlords are now taking the leap into remortgaging into a limited company too

Once, the notion of limited company buy-to-let was perceived to be a ‘niche within a niche’ and was merely deemed to be the preserve of bigger ‘corporate’ landlords with more complicated structures.

This has clearly changed, with the Government measures to reduce the amount of mortgage interest tax relief landlords could secure causing a huge shift towards the use of limited companies, not just for portfolio landlords but specifically for any landlord considering a new purchase.

Landlords were always going to seek out ways in which they could continue to maintain profitability, add to portfolios, etc, at a time when a number of previous incentives for investing were being taken away from them.

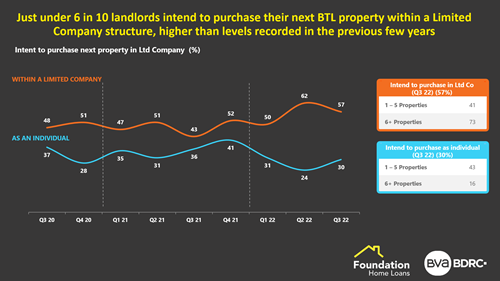

It seems likely that – based on the current taxation structure we can expect a high appetite for landlords to invest in the sector via a limited company. Indeed, this has been rising slowly: according to BDRC, six in ten landlords plan to make their next purchase in a limited company, whereas this was 5 in 10 only at the start of this year.

What we may see now is an increase in existing landlords who own the property in their individual name(s) beginning the process to move those homes into a limited company structure.

The benefits of buying within a limited company structure are well known, however, remortgaging an existing property held in an individual name into a limited company structure comes with more costs.

Now, this is a significant decision for any landlord, because it is defined as a change in ownership and is therefore subject to stamp duty. Landlords should be taking tax advice around this and weighing up any move against the stamp duty that will need to be paid.

It might be many thousands of pounds because of the 3% surcharge that comes with stamp duty costs for landlords, but there might be those who when they crunch the numbers – especially with the recent cut to stamp duty, over the long-term, it will end up saving them money because they are able to secure the full mortgage interest relief available within the corporate structure.

Many landlords have made the call that paying the stamp duty on a property you already own right now might not seem like a good move, and if the landlord only intends to maintain their investment for the short-term, then it might not be the right approach. However, if your landlord clients are in this sector for the long-term, and if they have plans to add to portfolios over that period, then they may be thinking now that moving existing properties into that structure now, could end up providing them with a long-term financial benefit.

As always, the advice to advisers is to make sure you don’t stray into tax advice here and having a strong relationship with a tax adviser yourself might provide another string to your bow in terms of helping such clients.

Whether it’s a newly-incorporated one or one with a more complex structure, solutions can be found for a part of the buy-to-let market that is becoming far more common and is likely to grow further as a method of investing in property.

Mark Whitear is Director of Commercial Development at Foundation Home Loans

FOR INTERMEDIARIES ONLY