Your Business and Industry

How to meet your self-employed clients’ shifting homeownership aspirations

On the back of such an uncertain period for many people, it’s vital for lenders to establish a real understanding of how people view their homes (whether rented or owned), how/why any views may have shifted and how people have adapted. Not to mention, future property objectives and their perceptions of the current mortgage market.

These questions – and many more – formed the basis of an exclusive Foundation Home Loans Housing Aspirations Report which was recently produced in conjunction with BVA BDRC. And we’d like to share some of the findings to try shed a little light on the sentiments of employed and self-employed people in regard to these aspirations, attitudes and potential barriers.

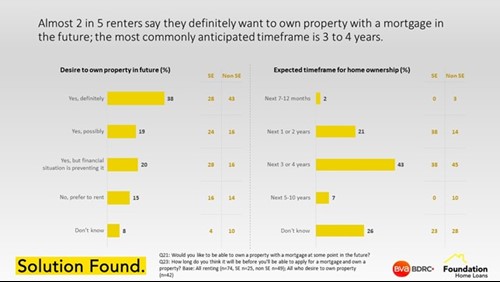

When surveying tenant respondents on their future outlook, almost two in five renters (38%) definitely want to own property with a mortgage at some point in the future, with the most commonly anticipated timeframe being three to four years. Interestingly, an additional 20% said that they would like to own a property but outlined that their financial situation was preventing this, a reason which 16% of employed rising to 28% of self-employed respondents indicated. A further 19% of tenants viewed home ownership as a possibility, and 15% said they preferred to stay renting.

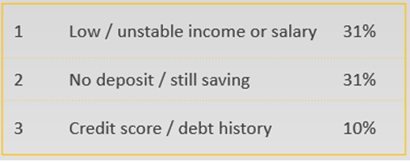

Staying with finances being the main barrier to owning a property, 31% cited a low/unstable income or salary as being the primary reason, an equal number said lack of deposit/still saving, with 10% suggesting that their credit score or debt history was the main barrier.

It’s clear from this data that homeownership aspirations remain strong across the UK. However, with many different types of financial hardships having occurred over the course of the pandemic for potential buyers – whether short, medium or longer-term – and many existing homeowners needing to utilise government support measures, additional layers of complexity are evident across the mortgage market. With policy, criteria and attitudes to risk differing from lender to lender, then the reliance on intermediary advice has further intensified, as has the amount of attention being focused on specialist residential lenders to meet these shifting client expectations.

So, if you would like to know more about how our specialist residential offering can help your clients, then speak to one of our team today.